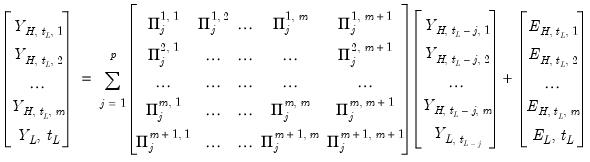

The VAR contains  variables

variables  , observed at low frequency and

, observed at low frequency and  variables

variables  observed at the high frequency. Let

observed at the high frequency. Let

variables , observed at low frequency and variables observed at the high frequency. Let variables , observed at low frequency and variables observed at the high frequency. Let  represent the i-th low frequency variable observed during low-frequency period

represent the i-th low frequency variable observed during low-frequency period

represent the i-th high frequency variable observed in the t-th high-frequency period during low-frequency period

represent the i-th high frequency variable observed in the t-th high-frequency period during low-frequency period

and

and  variables into the matrices

variables into the matrices  and

and  , respectively, and for brevity ignoring the intercepts and exogenous variables, we may write the VAR as:

, respectively, and for brevity ignoring the intercepts and exogenous variables, we may write the VAR as: | (49.1) |

is

is  ,

,  is

is  , and

, and  is

is  , for all

, for all  ,

,  , and

, and  is

is  .

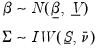

. , the stacked matrix of coefficients.

, the stacked matrix of coefficients. and the residual covariance matrix,

and the residual covariance matrix,  (

“Technical Background”).

(

“Technical Background”). | (49.2) |

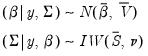

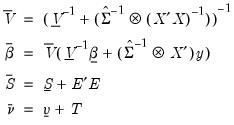

and

and  of:

of: | (49.3) |

(49.4) |

| (49.5) |

is constructed like the Litterman prior in standard Bayesian VARs.

is constructed like the Litterman prior in standard Bayesian VARs.  is assumed to be all zero, other than the own first lag terms. However the Ghysels prior differs slightly by allowing a different hyper-parameter for the own lag term depending on whether a variable is high or low frequency. Another crucial difference is that the variables are assumed to follow an AR(1) process in the high-frequency, so that when estimating in low-frequency space, the parameter is exponential.

is assumed to be all zero, other than the own first lag terms. However the Ghysels prior differs slightly by allowing a different hyper-parameter for the own lag term depending on whether a variable is high or low frequency. Another crucial difference is that the variables are assumed to follow an AR(1) process in the high-frequency, so that when estimating in low-frequency space, the parameter is exponential. is similar to a Litterman prior, but with subtle differences to allow for the cross-frequency variances.

is similar to a Litterman prior, but with subtle differences to allow for the cross-frequency variances. Element | Mean | Variance | Dimension |

|  |  |  , ,  |

|  |  |  |

| 0 |  |  , ,  , ,  |

| 0 |  |  , ,  |

| 0 |  |  , ,  , ,  |

| 0 |  |  , ,  |

| 0 |  |  , ,  |

,

,  ,

,  and

and  are hyper-parameters, and

are hyper-parameters, and  is a

is a  matrix with the (i,j)-th element equal to

matrix with the (i,j)-th element equal to  ,

,  ,

,  where the

where the  are taken from a univariate AR(1) estimation.

are taken from a univariate AR(1) estimation. .

. is formed by taking a scaled identity matrix or by scaling an initial estimate of the variance taken from a classical least squares U-MIDAS estimation:

is formed by taking a scaled identity matrix or by scaling an initial estimate of the variance taken from a classical least squares U-MIDAS estimation: | (49.6) |

or

or  .

.