Background

The TVCVAR consists of two equations, an observation equation and a process equation. The observation equation is a VAR equation with period-specific coefficients, and the process equation specifies a law of motion for the coefficients. The BTVCVAR combines the TVCVAR with a prior distribution over the initial state of the coefficients process and the model parameters.

Observation Equation

Let

denoted the

-vector of endogenous variables observed on date

for

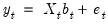

. To motivate the two equations that form the TVCVAR, we start with the basic VAR model. The VAR equation under the basic VAR is

where the covariate vector

| (48.1) |

consists of

lags of

and the vector of exogenous variables

. The coefficient matrix

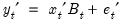

is constant over time. We can get rid of this assumption by adding a time subscript on

. Doing so yields the observation equation:

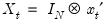

| (48.2) |

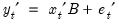

Vectorizing both sides of the observation equation gives

| (48.3) |

where

and

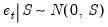

. The error vector

is given by

where

is the observation covariance matrix.

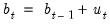

Process Equation

Making coefficients period-specific resolves the original problem, but introduces a new one: Taken alone, the observation equation results in a model that is over-parameterized for any sample size. We can mitigate this issue by specifying a law of motion for the coefficients. Typically this law of motion takes the form of a random walk process:

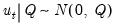

This is the process equation. The process error is given by

where

is the process covariance matrix. The initial state of this process,

, is specified as part of the prior.

Prior Distribution

The process equation is certainly helpful, but may not completely eliminate the problems that are associated with over-parameterization. Indeed, over-parameterization is often an issue even for the basic VAR. The usual solution is to “shrink” the model towards a simpler or stylized version of itself. The concept of shrinkage brings us to our next topic, the BTVCVAR.

The BTVCVAR combines the TVCVAR with a prior distribution. Bayesians form priors based on information they have on the subject under study prior to seeing the data. For many non-Bayesians, the prior is simply a means for achieving shrinkage. To shrink the model towards a simpler or stylized version of itself, center the prior at the simpler/stylized model. Tightening the prior will then pull estimates towards the model at the center of the prior.

One example of shrinkage was already mentioned; the TVCVAR can be made to shrink towards the basic VAR by specifying a tight prior about zero for the process error variance terms. Shrinking towards the basic VAR to some extent is desirable because it yields coefficient estimates that evolve more smoothly over time.

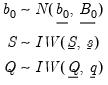

The prior over the initial coefficient vector

and covariance matrices

and

is

where

| (48.4) |

See the prior specification subsection for details on how to set the prior hyper-parameters.

The exposition here assumes an unrestricted process covariance matrix. In practice, it is more common to work with a diagonal

. See the implementation details section for more information.

Posterior Distribution

The prior distribution combines with the likelihood function to form the posterior distribution, which becomes the basis for inference, predictions, etc. For example, a Bayesian point estimate is usually just the mean or median of the posterior distribution.

Let

denote the set of all observed data, and let

denote the set of all coefficients including

. The posterior distribution over the model unknowns

,

, and

is given by

where the first, second, and third terms on the right-hand side of the proportionality symbol correspond to the prior distribution, the observation equation, and the process equation, respectively.

This distribution does not lend itself to vanilla Monte Carlo sampling. Fortunately, posterior simulation is possible using the Gibbs sampler. See

“Implementation Details” for additional information.