Cumulative standard deviations (d.f. adjusted) of a series.

Equivalent to @cumstdevs.

Increasing samples calculation of the square root of the sample (d.f. adjusted) Pearson product moment variance.

Syntax: @cumstdev(x, [s])

x: series

s: (optional) sample string or object

Return: series

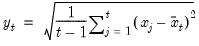

The sample standard deviation is calculated for each observation

as

where

is the mean of

over the first

observations.

This function is panel aware.

Examples

series x = @nrnd

group g @cumstdev(x) @cumstdevs(x) @cumstdevp(x)

g.line

plots @cumstdev(x), @cumstdevs(x), and @cumstdevp(x) together. Note that @cumstdev(x) and @cumstdevp(x) are equivalent. All three series converge in probability to 1.

Cross-references

For the backward cumulative variant of this function, see

@cumbstdev.