Testing and Diagnostics

The new estimators described in

“Estimation” all have various estimator-specific views for testing and diagnostics.

Seasonal Unit Root Testing

An important element of time series data is seasonality or cyclicality. Typically, seasonality is treated as a stationary feature in most time series models. Nevertheless, non-stationarity, particularly of the unit-root kind, can be an important feature within the cyclical components themselves, and can give rise to similar inferential inaccuracies and concerns one often encounters with traditional unit root series. Accordingly, identifying the presence of unit roots at one or more seasonal frequencies is the subject of the battery of tests known as seasonal unit root tests.

EViews 12 offers several seasonal unit root tests, including the classical Hylleberg, et al. (1990, HEGY) test, the Smith and Taylor (1999) likelihood ratio test, the Canova and Hansen (1995) test, the Taylor (2003) robust stationarity test, and the Taylor (2005) variance ratio test.

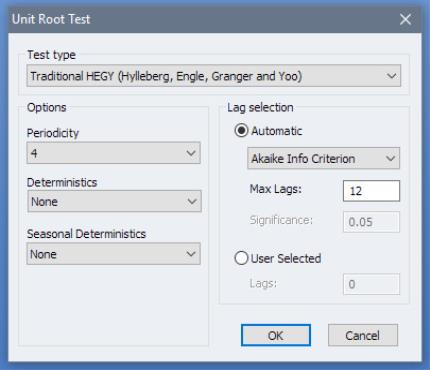

To begin, double click on a series name to open the series window. From there, select

You may choose between:

• Traditional Hylleberg, Engle, Granger, and Yoo (HEGY) test

• HEGY Likelihood Ratio test

• Canova-Hansen test

• Variance ratio test

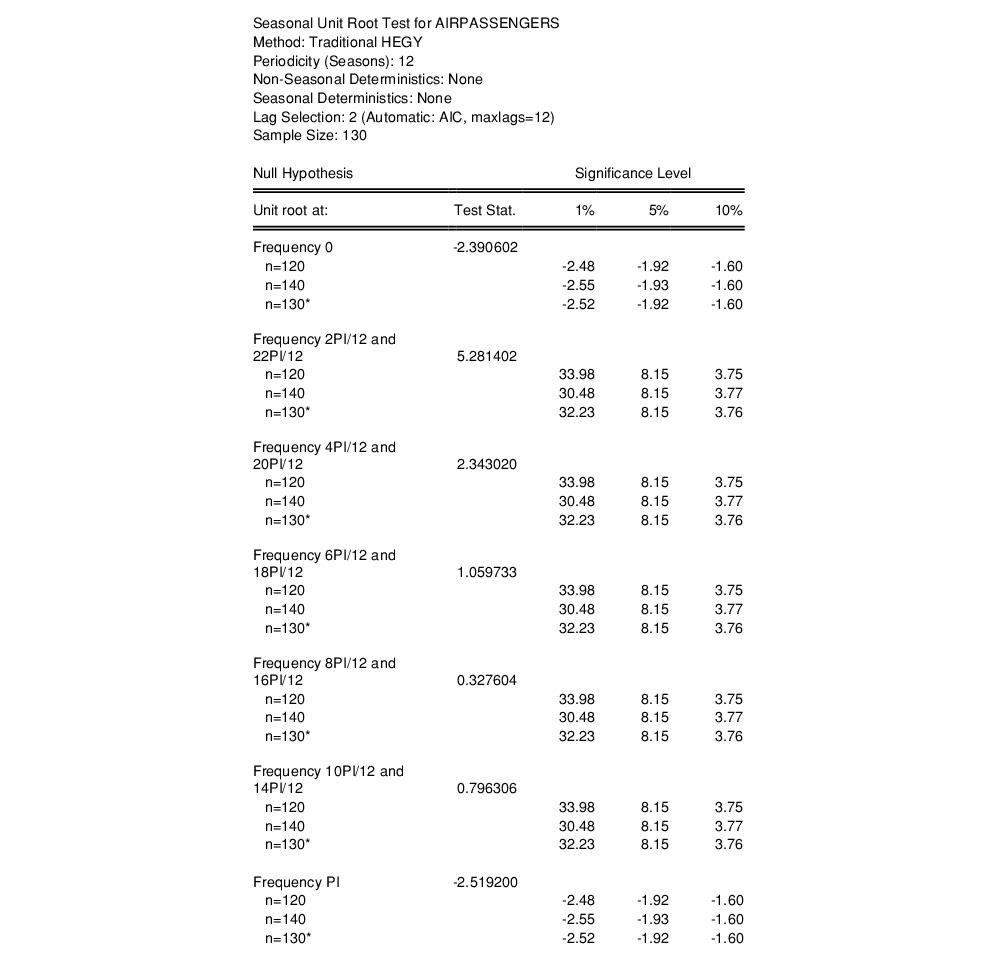

For example, results for a traditional HEGY test are of the form: